Hi Everyone,

<<UPDATE! I HAVE ATTACHED AN EXCEL-BASED CALCULATOR FOR THE MATHEMATICALLY CHALLENGED >>

>>

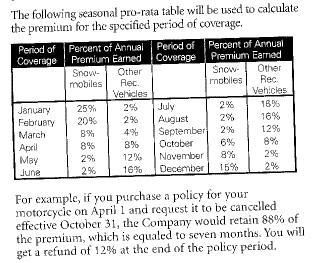

Time and time again, GTAM members ask me why they aren't allowed to cancel their State Farm policy (or drop to Fire and Theft only) for the winter without paying a "penalty". Although State Farm charges equal premiums every month, you actually "use up" the annual premium much faster over the Spring/Summer months than you do in the Fall/Winter. You are given the following copy of the State Farm premium-earning schedule with your policy package (note that a motorcycle is considered part of "Other Rec. Vehicles"):

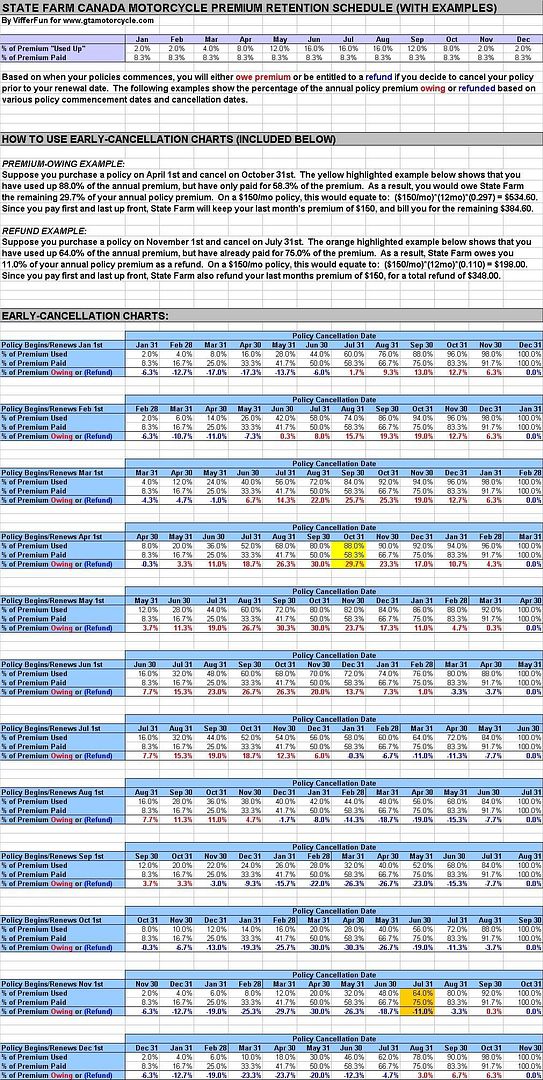

Depending on when your policy took effect and when you decide to cancel, you will fall into one of two categories:

Find the example below with the closest policy effective date to your own, and you can get an idea of what will happen should you decide to cancel your policy.

Enjoy!

<<UPDATE! I HAVE ATTACHED AN EXCEL-BASED CALCULATOR FOR THE MATHEMATICALLY CHALLENGED

>>Time and time again, GTAM members ask me why they aren't allowed to cancel their State Farm policy (or drop to Fire and Theft only) for the winter without paying a "penalty". Although State Farm charges equal premiums every month, you actually "use up" the annual premium much faster over the Spring/Summer months than you do in the Fall/Winter. You are given the following copy of the State Farm premium-earning schedule with your policy package (note that a motorcycle is considered part of "Other Rec. Vehicles"):

Depending on when your policy took effect and when you decide to cancel, you will fall into one of two categories:

- You OWE State Farm for premium that you "used up" but did not yet pay for

- You are entitled to a REFUND because you have paid for more premium than you have "used up"

- January 1st

- February 1st

- March 1st

- April 1st

- May 1st

- June 1st

- July 1st

- August 1st

- September 1st

- October 1st

- November 1st

- December 1st

Find the example below with the closest policy effective date to your own, and you can get an idea of what will happen should you decide to cancel your policy.

Enjoy!

Attachments

Last edited: