EDIT: This posting has been corrected and should hopefully be accurate.

EDIT: This posting is only intended for TD / MM / Primmum customers that are on the 7-month payment plan. If you are on a 12-month payment plan, then your policy has been grandfathered from an old Liberty Mutual account and this posting does not apply to you.

Hi Everyone,

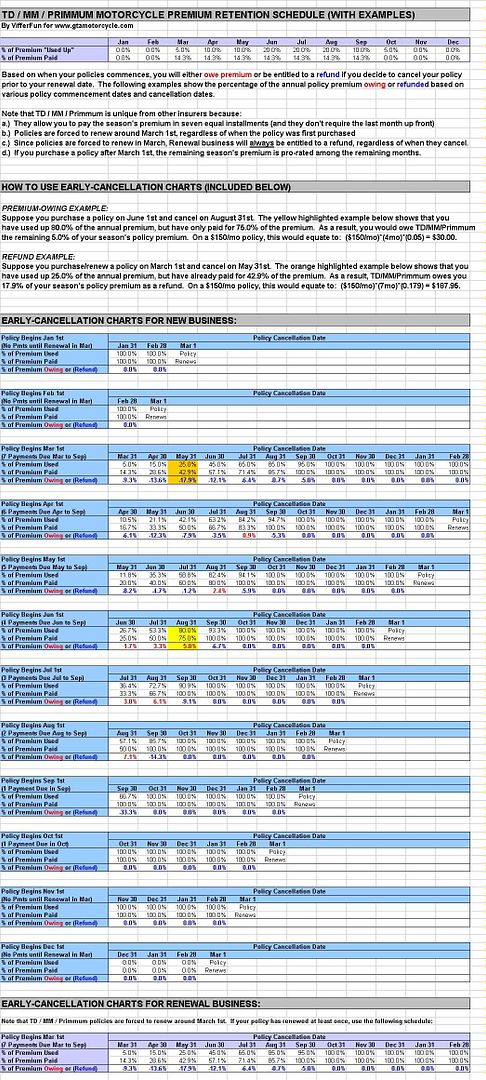

Time and time again, GTAM members ask me why they aren't allowed to cancel their TD/MM/Primmum policy (or drop to Fire and Theft only) without paying a "penalty". Although TD/MM/Primmum charges equal premiums every month from March to September (i.e. 7 months), you actually "use up" the annual premium much faster over the Summer months than you do in the Spring/Fall months. TD/MM/Primmum uses the following premium-earning schedule for Motorcycles:

Although I work in the insurance industry, I do not work for TD/MM/Primmum; however, based on their premium-earning schedule, I have put together the following document to help people understand what they will owe (or be refunded) should they decide to cancel their policy early. The twelve new business examples and one renewal example I have created below are for the following specific policy effective/renewal dates:

If your policy has not yet renewed, find the New Business example below with the closest policy effective date to your own, and you can get an idea of what will happen should you decide to cancel your policy. If your policy has already renewed at least once, refer to the single "Renewal Business" example.

Enjoy!

EDIT: This posting is only intended for TD / MM / Primmum customers that are on the 7-month payment plan. If you are on a 12-month payment plan, then your policy has been grandfathered from an old Liberty Mutual account and this posting does not apply to you.

Hi Everyone,

Time and time again, GTAM members ask me why they aren't allowed to cancel their TD/MM/Primmum policy (or drop to Fire and Theft only) without paying a "penalty". Although TD/MM/Primmum charges equal premiums every month from March to September (i.e. 7 months), you actually "use up" the annual premium much faster over the Summer months than you do in the Spring/Fall months. TD/MM/Primmum uses the following premium-earning schedule for Motorcycles:

- JAN: 0.0%

- FEB: 0.0%

- MAR: 5.0%

- APR: 10.0%

- MAY: 10.0%

- JUN: 20.0%

- JUL: 20.0%

- AUG: 20.0%

- SEP: 10.0%

- OCT: 5.0%

- NOV: 0.0%

- DEC: 0.0%

- You OWE TD/MM/Primmum for premium that you "used up" but did not yet pay for

- You are entitled to a REFUND because you have paid for more premium than you have "used up"

Although I work in the insurance industry, I do not work for TD/MM/Primmum; however, based on their premium-earning schedule, I have put together the following document to help people understand what they will owe (or be refunded) should they decide to cancel their policy early. The twelve new business examples and one renewal example I have created below are for the following specific policy effective/renewal dates:

- January 1st

- February 1st

- March 1st

- April 1st

- May 1st

- June 1st

- July 1st

- August 1st

- September 1st

- October 1st

- November 1st

- December 1st

If your policy has not yet renewed, find the New Business example below with the closest policy effective date to your own, and you can get an idea of what will happen should you decide to cancel your policy. If your policy has already renewed at least once, refer to the single "Renewal Business" example.

Enjoy!

Last edited:

")